Subjects

Grades

The fridge is almost empty, and it’s nearly supper time. You better go to the grocery store. While shopping, you notice that the prices on some foods have changed since your last visit. Why?

How are sales prices determined? There is a whole process that goes on behind the scenes before a price is printed on a label at the grocery store: the law of supply and demand.

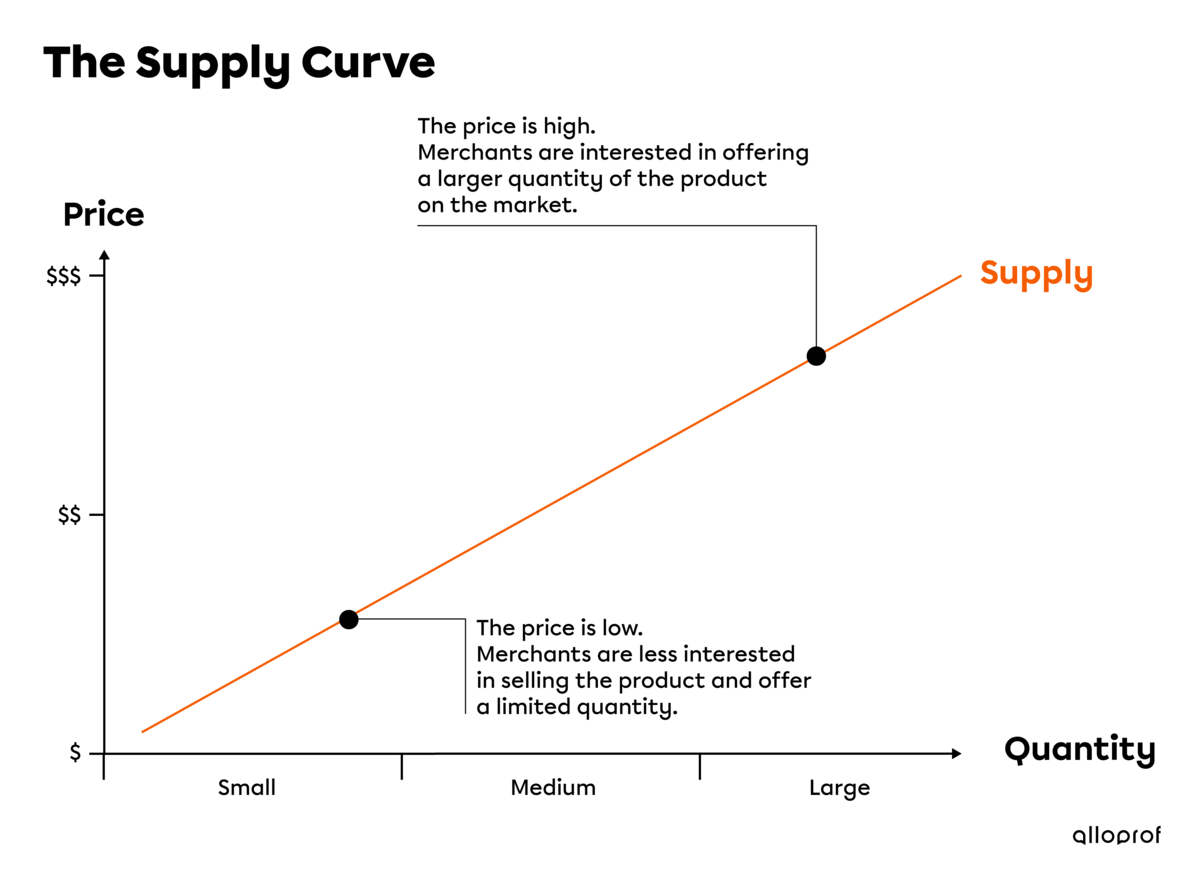

Supply refers to the quantity of goods or services that merchants offer based on the sales price. The higher the price, the better it is to offer the goods or services. The money earned will pay for expenses incurred during production and sales, and it will also lead to higher profits.

As an example, merchants might choose to sell many types of goods if the sales price on one product is too low to pay for the expenses incurred to produce and sell them. If the cost to the merchant is more than the price sold to the consumer, there is no reason to offer that product.

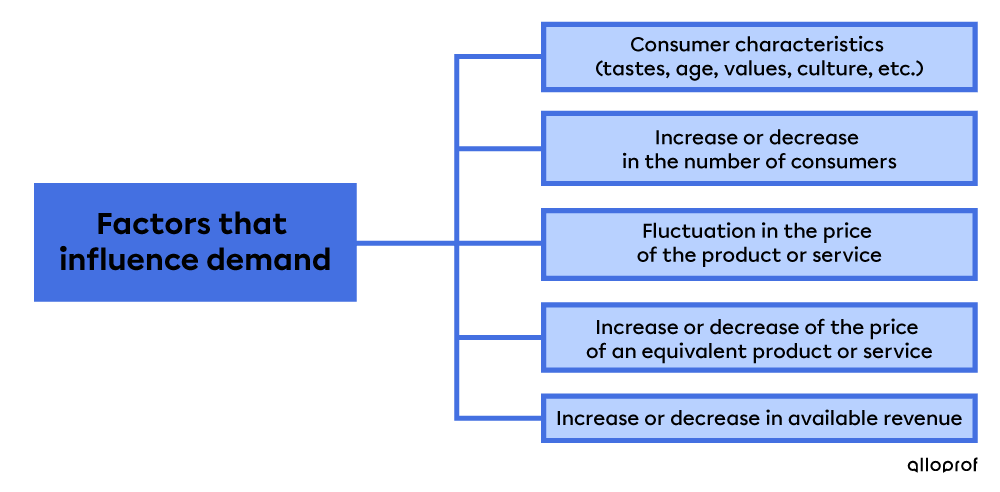

Demand refers to the quantity of goods or services that consumers are willing to buy for a given price. This is the quantity that consumers demand from merchants.

Each consumer will consider their financial resources when evaluating the price of goods and services. If the price of a product is very high, a person may not be high enough for them to be able to afford it. If people feel that a product is too expensive, they are not likely to buy it.

If onions cost $8.00 each, buying onions might be too expensive for your budget. You may want to wait to buy them or replace them with a less expensive vegetable, like celery.

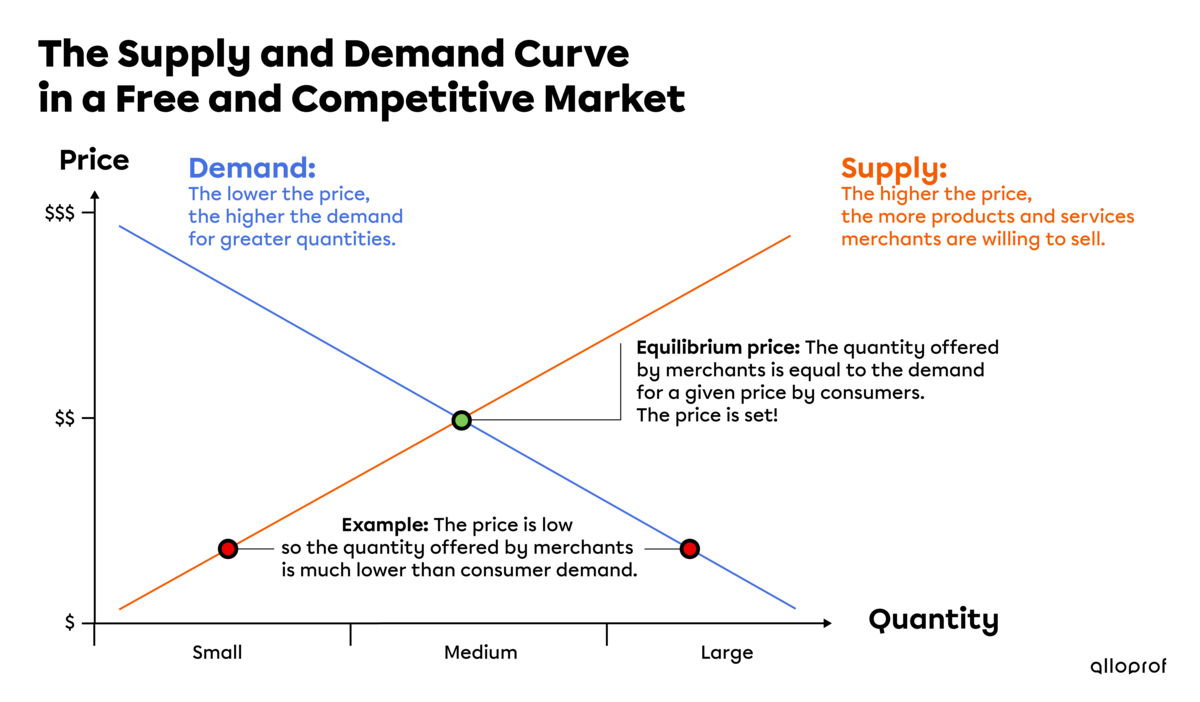

Pricing is determined based on the balance between supply and demand for a product or service. The price of onions fluctuates several times before reaching a price that is “just right.” The price set is a balance between what consumers are willing to pay for an onion and the price at which merchants are willing to sell it.

The equilibrium price is the price at which the merchant (supply) is willing to sell goods and the consumer (demand) is willing to pay for a given quantity of goods.

In the graph, the example with the red dots shows that, for the same price, there is a big difference between the quantity demanded and the quantity supplied.

If the price is low, the consumers’ demand for the product is high because they can buy more.

However, a low price means merchants are less interested in offering the product, because lower profits can jeopardize their businesses.

The quantity offered by merchants becomes much lower than the quantity demanded by consumers.

Production costs refer to the money needed to produce goods or services in terms of materials, labour, equipment and facilities, among others.

When evaluating supply, merchants look at the costs required:

to produce the goods and services

to provide goods and services to consumers

If an onion costs $2 to produce (seeds, fertilizer, time, machinery, etc.), the producer will try to sell it for more than $2 in order to cover the production costs while making a profit at the same time.

Merchants must also adjust to the sales price set by other merchants.

For example, the convenience store on Monkland Street sells onions for $1.50 each. The convenience store on Atwater Street sells onions for $3.00 each. The one on Monkland is more likely to get your business because its onions are half the price of the ones at the store on Atwater.

The equilibrium price changes over time and in different situations, so when you buy onions or any other product or service, their price can vary from month to month.

There are several factors that can influence demand and the equilibrium price:

Disposable income is the amount of money a person has left after paying all of their mandatory expenses, like rent, utility bills and groceries, for a given period.

There are various factors that influence producers’ and merchants’ supply: